Em meio à reestruturação em curso das cadeias de suprimentos globais, o Camboja está emergindo rapidamente como uma potência emergente na fabricação de bolsas. Fabricantes de bolsas do Vietnã Embora a China seja há muito considerada referência para a indústria manufatureira do Sudeste Asiático, os dados mais recentes revelam que o Camboja está demonstrando vantagens competitivas únicas no setor de artigos de viagem. Em 2025, as exportações de bolsas do Camboja ultrapassaram US$ 2 bilhões, com todo o setor de vestuário, calçados e artigos de viagem (GFT) atingindo um recorde histórico de US$ 16 bilhões em exportações totais.

Este artigo oferece uma análise aprofundada das cinco principais vantagens que o Camboja possui em relação às fábricas de bolsas do Vietnã, fornecendo informações baseadas em dados para auxiliar nas suas decisões de cadeia de suprimentos.

O salário mínimo no Camboja é de apenas US$ 210 por mês (padrão de 2026), significativamente inferior a fábricas de bolsas do Vietnã custos trabalhistas atuais. Apesar dos ajustes anuais feitos pelo governo cambojano (o aumento em 2026 foi de apenas US$ 2, chegando a US$ 210), essa abordagem gradual equilibra o bem-estar dos trabalhadores com a competitividade dos custos industriais.

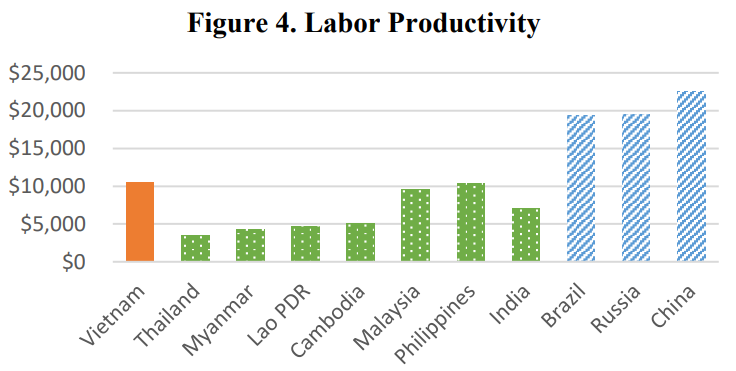

Para produtos que demandam muita mão de obra, como bolsas, essa diferença de custo se traduz diretamente em uma vantagem de custo de fabricação de 15 a 20% em relação aos fabricantes de bolsas do Vietnã. Notavelmente, a produtividade do trabalho no Camboja continua a aumentar de forma constante, com a produtividade do setor industrial atingindo US$ 2.424 por trabalhador em 2019.

Isso representa o diferencial estratégico mais valioso do Camboja em comparação com Fabricantes de bolsas do Vietnã.

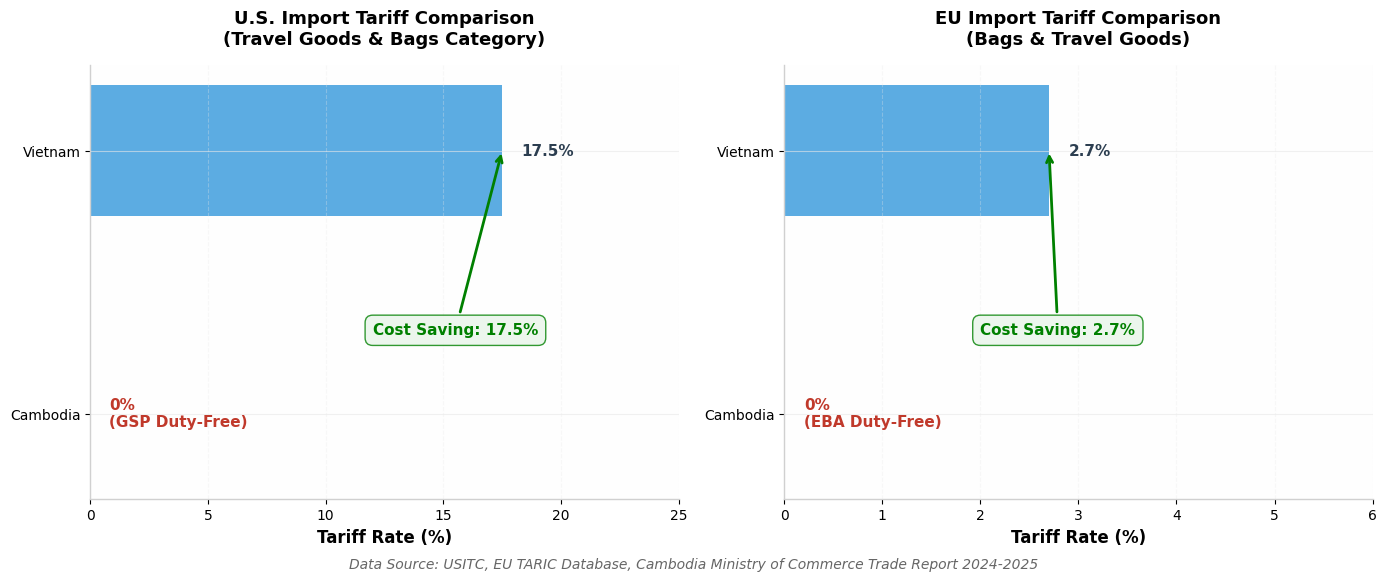

Desde 2016, o Camboja goza do status de SGP (Sistema Geral de Preferências) dos EUA, o que permite a entrada de artigos de viagem (incluindo malas, mochilas, bolsas e carteiras) no mercado americano sem impostos. Em contrapartida, produtos similares fabricados no Vietnã estão sujeitos a tarifas de NMF (Nação Mais Favorecida) que variam de 10% a 30%.

Mesmo com a tarifa de 19% imposta pelos EUA ao Camboja em 2025, as vantagens em termos de custo de mão de obra permitem que a fabricação de bolsas no Camboja permaneça competitiva com os fabricantes de bolsas do Vietnã e da Tailândia. Além disso, o Camboja se beneficia de:

Esses acordos comerciais preferenciais proporcionam aos exportadores de bolsas uma economia de custos de 12 a 33% nas despesas tarifárias em comparação com as fábricas de bolsas do Vietnã.

Quantificação dos Custos Tarifários: Esta é a comparação mais direta da competitividade de custos em relação às fábricas no Vietnã. No mercado americano, as bolsas cambojanas têm isenção de impostos sob o Sistema Geral de Preferências (SGP), enquanto os produtos fabricados no Vietnã estão sujeitos a uma tarifa média de 17,5% (variando de 10% a 30%) com base no princípio da Nação Mais Favorecida (NMF).

O mercado da UE é igualmente favorável: ao abrigo do regime EBA, o Camboja beneficia de tarifas zero no mercado da UE; enquanto os fabricantes de malas do Vietname, apesar das vantagens do EVFTA, continuam a pagar uma taxa média de 2,7%. Para a indústria de malas, com margens reduzidas, esta diferença de 2,7% é substancial em grande escala.

Nota sobre riscos: Embora a política do Sistema Geral de Preferências (SGP) dos EUA apresente incertezas (historicamente intermitentes), a fabricação de bolsas no Camboja mantém a competitividade geral de custos com as fábricas de bolsas do Vietnã, mesmo sob o cenário de tarifa de 19% em 2025, graças às vantagens de custo de mão de obra. Além disso, os benefícios do programa EBA da UE estão garantidos pelo menos até 2029, proporcionando segurança para o planejamento de médio a longo prazo.

O Camboja estabeleceu polos industriais dedicados aos setores de vestuário, calçados e artigos de viagem. Em 2024, o país abrigava aproximadamente 1.600 fábricas desse setor, empregando mais de 800.000 trabalhadores, dos quais 75,5% eram mulheres.

Ao contrário da ampla base de produção das fábricas de bolsas do Vietnã, o Camboja desenvolveu divisões altamente especializadas na fabricação de bolsas:

No âmbito da Estratégia de Desenvolvimento Industrial GFT do Camboja para 2022-2027, o governo está a promover ativamente a modernização das fábricas, passando de modelos puramente CMT (Corte-Fabricação-Aparamento) para capacidades OEM/ODM. Isto significa que as fábricas cambojanas agora possuem a capacidade de desenvolver projetos e aceitar encomendas de alto valor acrescentado, rivalizando com as fábricas sediadas no Vietname.

Em comparação com a estrutura das fábricas de bolsas do Vietnã, dominada por megafábricas, a escala das fábricas do Camboja é mais flexível, proporcionando vantagens exclusivas para lotes menores, maior variedade de estilos e prazos de entrega mais rápidos para pedidos de bolsas.

Os dados mostram que as quantidades mínimas de encomenda (MOQs) típicas das fábricas cambojanas variam de 3.000 a 5.000 peças por modelo. Empresas como a SYNBERRY BAG CAMBODIA conseguem atender aos requisitos de qualidade e capacidade das principais marcas, mantendo ao mesmo tempo flexibilidade na fabricação OEM/ODM para pequenas e médias empresas que buscam alternativas à produção chinesa e às grandes fábricas do Vietnã.

O governo cambojano considera o setor manufatureiro um pilar da economia, com a projeção de crescimento de 8,6% para o setor industrial em 2025, marcando o segundo ano consecutivo de crescimento acima de 8%. Essa estabilidade política oferece garantias para investimentos de longo prazo.

Em comparação com a exposição do setor de fabricação de bolsas do Vietnã aos riscos de atrito comercial, o Camboja mantém o status de País Menos Desenvolvido (PMD) até 2029, desfrutando de tratamento especial no comércio internacional durante esse período de transição. Mesmo após deixar de ser um PMD, o Camboja pode manter o acesso ao mercado da UE com tarifa zero por meio de programas GSP+ em conformidade, desde que os padrões de direitos humanos e ambientais sejam atendidos — alinhando-se perfeitamente com as propostas de valor de uma marca responsável.

Conclusão: Camboja — A posição estratégica ideal para a fabricação de bolsas em comparação com os fornecedores vietnamitas.

Para marcas de bolsas que buscam otimização de custos, vantagens tarifárias e capacidade flexível, o Camboja oferece uma proposta de valor que muitos fornecedores vietnamitas têm dificuldade em replicar. Particularmente no mercado americano, os benefícios da tarifa zero do Sistema Geral de Preferências (SGP) (caso a política seja mantida) podem se traduzir diretamente em uma competitividade de preço de 10 a 30% em relação às importações do Vietnã.

Os dados oficiais de importação e exportação confirmam as vantagens da indústria de fabricação do Camboja sobre a do Vietnã: nos últimos cinco anos, as exportações de artigos de viagem do Camboja apresentaram um crescimento exponencial, saltando de US$ 1,25 bilhão em 2020 para US$ 2 bilhões em 2025 — um aumento acumulado de 60%. Em contrapartida, embora o Vietnã mantenha vantagens absolutas em volume (US$ 4,8 bilhões), o crescimento desacelerou significativamente, com um aumento total de apenas 26% nos últimos 5 anos, indicando sinais de saturação do mercado já em 2021.

Embora as fábricas vietnamitas ainda possuam vantagens em termos de sofisticação da infraestrutura, para produtos de bolsas que exigem muita mão de obra, são relativamente padronizados e são exportados principalmente para os mercados dos EUA e da UE. O Camboja, sem dúvida, representa a escolha mais estratégica e voltada para o futuro em comparação com as opções tradicionais de fornecimento no Vietnã.

Portanto, para marcas que avaliam o layout da cadeia de suprimentos, recomendamos uma estratégia de base dupla "China + Camboja": manter os requisitos de produção de alta complexidade ou alta flexibilidade na China, enquanto transfere as linhas de produção de bolsas padronizadas para o Camboja, a fim de maximizar os benefícios tarifários e as vantagens de custo em relação às opções de fabricação no Vietnã.

Quer esteja a considerar transferir encomendas existentes de fábricas de malas no Vietname ou a estabelecer capacidade de produção no Sudeste Asiático pela primeira vez, a nossa equipa presta apoio integral — desde auditorias às fábricas e desenvolvimento de amostras até à produção em massa e entrega.

Entre em contato conosco hoje mesmo:

E-mail: [email protected]

WhatsApp: +86-139-5921-4481

(Todas as fontes de dados: Ministério do Comércio do Camboja, EuroCham Camboja, GMAC (Associação de Fabricantes de Vestuário do Camboja), Relatório do Observatório da Indústria de Vestuário Asiático (2024-2025)

Continue lendo, mantenha-se informado, inscreva-se e convidamos você a nos dizer o que você pensa.

Direitos autorais

@2024 Synberry Bag & Package Products Co.,Ltd Todos os direitos reservados

.

SUPORTADO POR REDE

SUPORTADO POR REDE